Economicspost

Post-Capitalist Economic System: Humanism

Humanism is a post capitalist economic system that places the value of human life above materialistic priorities such as capital, property, and the accumulation of wealth

351

A closer look at how housing, education, food, healthcare, and wages have changed since the 1970s—and what the numbers actually tell us when adjusted for inflation.

For many Americans, the feeling that life has become more expensive extends far beyond a single purchase or monthly bill. Buying a home, paying for college, raising a family, or even covering everyday necessities can seem significantly more difficult than it did for previous generations. These concerns have become a common topic of conversation both online and offline, with younger generations often questioning whether the economic opportunities enjoyed by their parents and grandparents are still within reach today.

Comparisons between the past and the present, however, can sometimes be misleading. Looking only at sticker prices ignores one important reality: a dollar in 1970 did not have the same purchasing power as a dollar today. Inflation has steadily increased prices across the entire economy over the past several decades. To make meaningful comparisons, economists adjust historical prices into today's dollars, allowing us to compare purchasing power rather than simply comparing numbers printed on price tags.

When prices are adjusted for inflation, an interesting picture begins to emerge. Many everyday goods have increased in price at roughly the same pace as inflation, meaning they consume a similar share of household income today as they did decades ago. Other expenses, however, have risen far faster than inflation itself. Housing, college tuition, childcare, and many healthcare costs have experienced increases that substantially outpaced both inflation and wage growth, placing increasing pressure on household budgets.

This article examines several of the largest expenses facing American households—including housing, education, food, healthcare, and wages—using inflation-adjusted figures whenever possible. Rather than relying on anecdotes or viral social media comparisons, the goal is to compare equivalent dollars across time and understand which costs have genuinely become more expensive, which have remained relatively stable, and how these changes have affected the financial lives of millions of Americans.

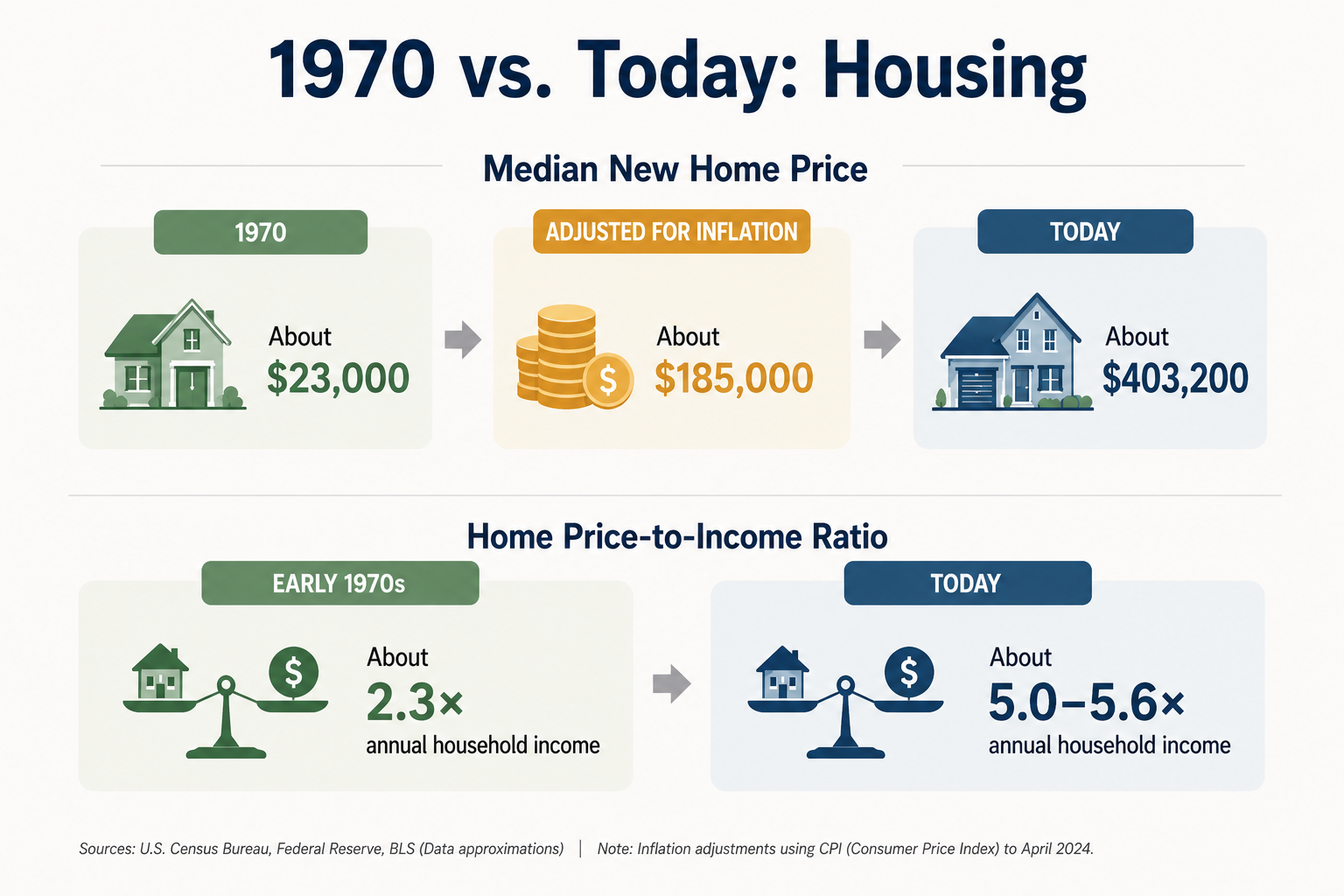

Housing is one of the clearest examples of a cost that has increased faster than inflation. In 1970, the median new home in the United States sold for approximately $23,000. Adjusted for inflation, that is roughly $180,000–190,000 in today's dollars. By comparison, the median new home sold in early 2026 costs approximately $403,200—more than twice the inflation-adjusted price of a comparable home in 1970. While homes today are generally larger and often include more modern amenities, the increase in price extends well beyond inflation alone.

Source: https://fred.stlouisfed.org/series/MSPUS

Income has also increased over the past five decades, but not nearly enough to keep pace with housing. The median family income in 1970 was $9,870, equivalent to roughly $82,000 in today's dollars after inflation. Modern median household income is now in the neighborhood of $80,000–85,000, meaning that inflation-adjusted incomes have grown only modestly while home prices have risen dramatically faster. As a result, the typical American household today must devote a much larger portion of its lifetime earnings toward purchasing a home than previous generations.

Source: https://www.census.gov/library/publications/1971/demo/p60-80.html

Economists often compare housing affordability by measuring how many years of median household income are required to purchase the median home. This removes the effects of inflation and allows for a more meaningful comparison across generations. During the early 1970s, the typical home cost approximately 2.3 times the median household income. By 2022, that figure had climbed to 5.6 times household income—the highest ratio recorded since national records began in the early 1970s.

This ratio illustrates why many younger Americans feel homeownership has become increasingly difficult. Even though incomes have generally kept pace with inflation, housing prices have grown much faster. Saving for a down payment now requires a significantly larger share of household income, while larger mortgages translate into higher monthly payments over the life of the loan. Combined with rising property taxes, insurance premiums, and higher interest rates in recent years, the financial barrier to buying a first home has become substantially higher than it was for many previous generations.

Source: https://www.jchs.harvard.edu/blog/home-price-income-ratio-reaches-record-high-0

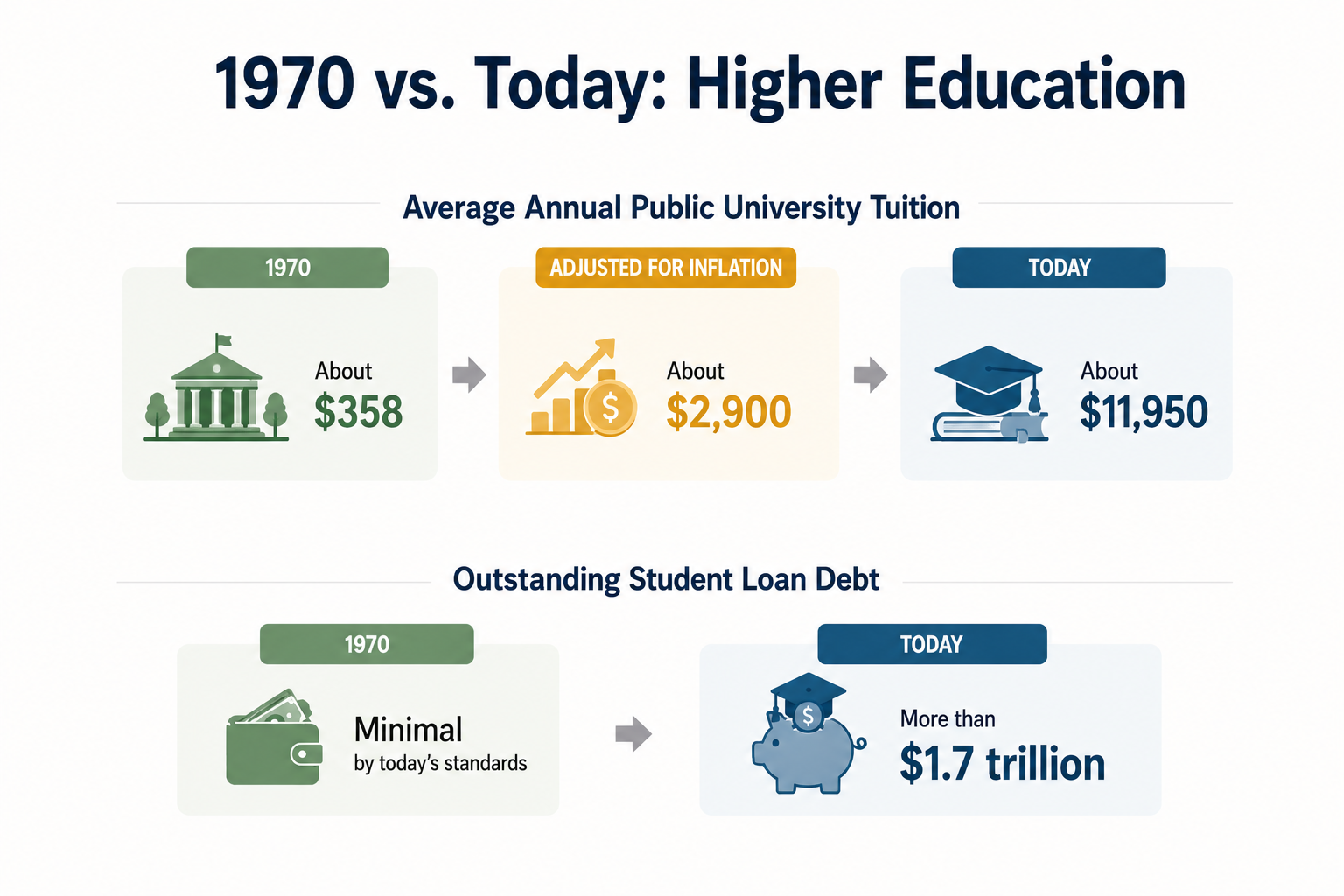

The cost of attending college has changed more dramatically than almost any other major household expense over the past fifty years. In the early 1970s, annual tuition and required fees at a four-year public university averaged approximately $394. Adjusted for inflation, that is roughly $3,100 in today's dollars. Today, the average published in-state tuition and required fees at a four-year public university are approximately $11,600 per year, nearly four times higher than the inflation-adjusted cost in the early 1970s. Private universities have experienced similar increases, with average tuition and fees now exceeding $43,000 per year before room and board.

Source: https://research.collegeboard.org/trends/college-pricing

These increases have significantly changed how students and families pay for higher education. While grants, scholarships, and financial aid reduce costs for many students, the published price of college has risen much faster than both inflation and household income. As a result, student borrowing has become far more common than it was for previous generations. Americans now owe more than $1.7 trillion in student loan debt, making education debt one of the largest categories of household debt in the United States.

Source: https://www.federalreserve.gov/

The increase in tuition has also changed the financial decisions many young adults make after graduation. Larger student loan balances can delay purchasing a first home, starting a business, saving for retirement, or building emergency savings. Although a college degree continues to increase average lifetime earnings, the upfront investment required to obtain that degree has grown substantially compared to previous generations.

Source: https://educationdata.org/average-cost-of-college

Researchers attribute rising tuition to several overlapping factors, including declining state funding for many public universities, increased demand for higher education, expanded campus services, administrative growth, and greater access to student loans. Economists continue to debate the relative importance of each factor, but there is broad agreement that tuition has increased considerably faster than both inflation and median household income over the past five decades.

Source: https://nces.ed.gov/

Unlike housing and higher education, grocery prices have generally tracked inflation more closely over the past fifty years. Many staple foods—including milk, bread, eggs, and chicken—cost significantly more today in dollar terms, but much of that increase reflects the declining purchasing power of the dollar rather than an extraordinary rise in food prices. The exception came during the inflation surge of 2021–2023, when grocery prices increased rapidly over a short period, placing additional strain on household budgets before inflation began to moderate.

Source: https://www.ers.usda.gov/data-products/food-price-outlook/

Even if many grocery items have roughly kept pace with inflation over the long run, food still represents a growing financial concern for many households because it is competing with other expenses that have increased much faster. Higher housing costs, insurance premiums, childcare expenses, and student loan payments leave less disposable income available for groceries, making food feel more expensive even when many staple prices have not dramatically outpaced inflation over several decades.

Source: https://www.bls.gov/cpi/

Although many staple foods have remained relatively close to their inflation-adjusted historical prices, consumers purchase far more than basic ingredients. Prepared meals, restaurant dining, packaged convenience foods, beverages, and delivery services now account for a much larger share of household food spending than they did several decades ago. These categories often experience different pricing pressures than raw agricultural products and can increase food budgets substantially.

Source: https://www.ers.usda.gov/data-products/food-expenditure-series/

In addition, shoppers tend to notice grocery prices because they encounter them every week. Unlike a mortgage or college tuition, grocery purchases are frequent and highly visible, making changes in food prices feel immediate. While food inflation certainly affects household budgets, long-term economic data suggest that housing, education, and healthcare have generally experienced much larger inflation-adjusted increases over the past fifty years than groceries.

Source: https://www.ers.usda.gov/data-products/food-price-outlook/

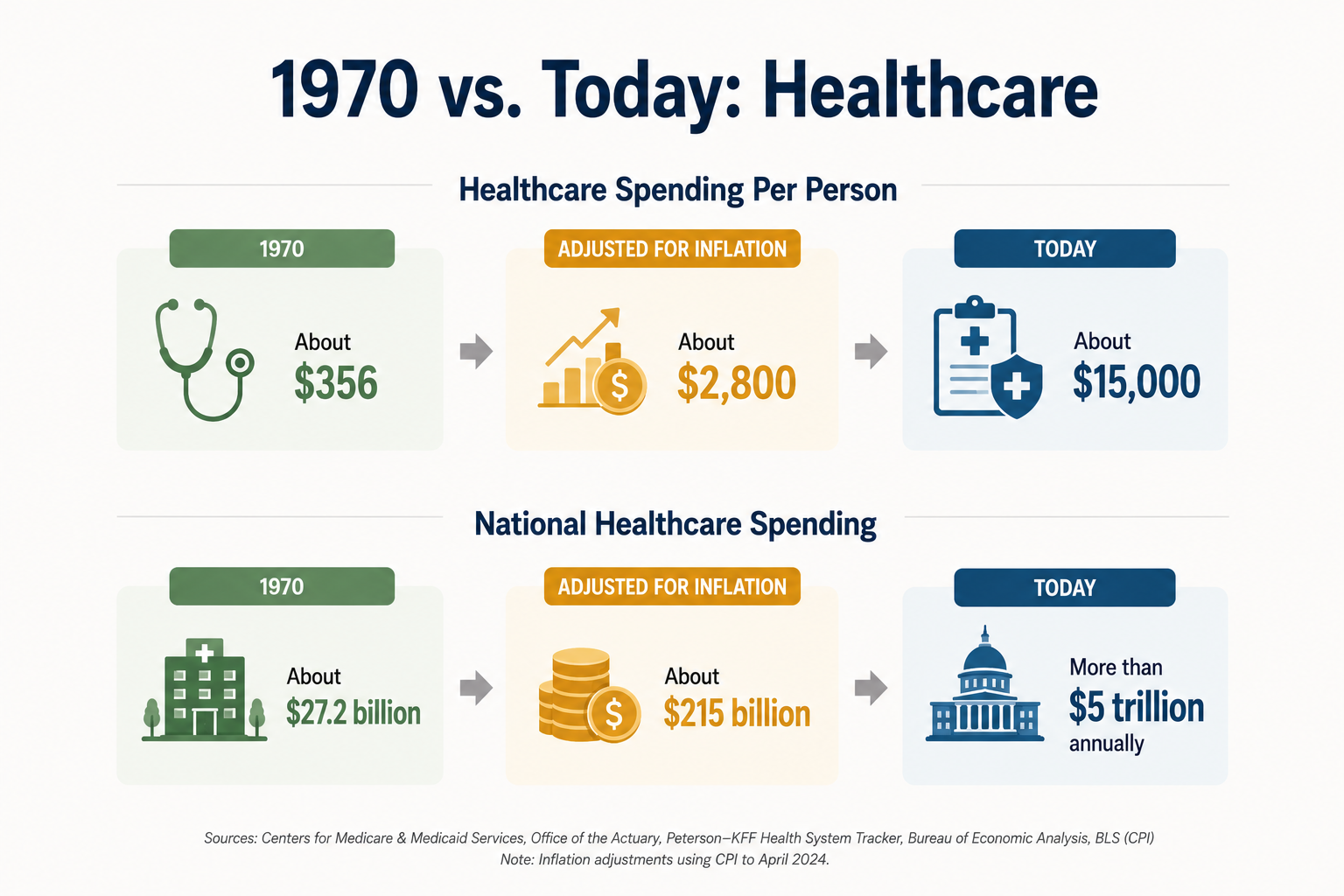

Healthcare has become one of the fastest-growing household expenses in the United States over the past fifty years. While advances in medicine have led to better treatments, improved survival rates, and new technologies, the cost of paying for healthcare has increased far faster than inflation. Today, Americans spend more on healthcare per person than any other developed nation, and medical costs consume a much larger share of household and government budgets than they did in the 1970s.

Source: https://www.cms.gov/data-research/statistics-trends-and-reports/national-health-expenditure-data

For many families, the increase is felt through monthly insurance premiums, deductibles, prescription drug costs, and out-of-pocket medical bills. Even households with employer-sponsored health insurance often pay thousands of dollars each year before insurance begins covering many services. These rising costs leave families with less income available for housing, education, retirement savings, and other essential expenses.

Source: https://www.kff.org/health-costs/

Healthcare spending has grown for many reasons. Americans are living longer, chronic diseases such as diabetes and heart disease have become more common, and modern medicine now offers treatments that simply did not exist decades ago. At the same time, hospitals, pharmaceutical companies, medical device manufacturers, insurers, and healthcare providers all contribute to a complex system with significant administrative costs. These factors have combined to push healthcare spending well beyond the rate of inflation.

Source: https://www.cms.gov/data-research/statistics-trends-and-reports/national-health-expenditure-data

Although healthcare costs have risen dramatically, health outcomes have not always improved at the same pace. The United States spends considerably more per person on healthcare than other high-income countries while continuing to debate how best to provide affordable access to care. This has led policymakers to explore a wide range of reforms, including expanding public insurance programs, increasing price transparency, reducing administrative costs, and negotiating prescription drug prices.

While wages have increased significantly in dollar terms since the 1970s, much of that growth reflects inflation rather than a dramatic increase in purchasing power. When adjusted for inflation, median household income has grown only modestly over the past five decades. For many workers, this means that although paychecks are larger than they were a generation ago, they have not increased enough to keep pace with the rising costs of housing, higher education, healthcare, and other major expenses.

Source: https://www.census.gov/topics/income-poverty/income.html

This helps explain why many Americans feel financially stretched despite earning more than previous generations. The issue is not simply that wages have remained stagnant, but that some of life's largest expenses have grown much faster than incomes. As a result, many households devote a greater share of their earnings to essential needs, leaving less room for savings, homeownership, retirement, or unexpected emergencies.

Source: https://www.epi.org/publication/charting-wage-stagnation/

Income growth has not been evenly distributed across the workforce. While average wages have increased over time, gains have been much stronger for higher-income earners than for many middle- and lower-income workers. At the same time, productivity has continued to rise, leading economists to debate how the benefits of economic growth have been shared across different groups of workers.

Source: https://www.epi.org/productivity-pay-gap/

Looking at wages alongside housing, education, and healthcare helps put the broader affordability discussion into context. Many Americans are not simply paying more because of inflation—they are facing a situation where several of the largest household expenses have risen considerably faster than income growth. Understanding this relationship provides an important foundation for exploring the policy ideas and public investments that could improve affordability in the decades ahead.

Source: https://fred.stlouisfed.org/

Looking at each expense individually only tells part of the story. Groceries have generally remained close to inflation over the long term, but housing, higher education, and healthcare have increased much faster. At the same time, household incomes have risen only modestly after adjusting for inflation. The result is that many families now spend a much larger share of their income on a handful of essential services than previous generations did, leaving less money available for savings, retirement, or discretionary spending.

This is why many Americans feel that the cost of living has become increasingly difficult, even when economic indicators suggest wages have grown over time. The issue is not simply that prices have increased—it is that several of the largest and most important household expenses have risen much faster than both inflation and income. Understanding this distinction is essential when discussing affordability and evaluating proposals to improve economic opportunity.

If the greatest pressure on household budgets comes from housing, education, and healthcare, then those are also the areas where thoughtful public investment has the potential to make the greatest difference. Around the world, many countries invest directly in affordable housing, public universities, healthcare systems, transportation, and other essential infrastructure to reduce the cost of living for their residents. While every country takes a different approach, the underlying goal is often the same: lowering the cost of essential services rather than simply increasing individual incomes.

Throughout Dream Cloud, we'll explore how different public investment models have been used around the world and examine what lessons they might offer for the United States. From expanding affordable housing and investing in education to strengthening public healthcare and building long-term public wealth, we'll look at how governments can help reduce financial pressure on households while creating stronger, more resilient communities. Rather than asking only how people can earn more, we'll also explore how society can make the things people need most more affordable in the first place.

Humanism is a post capitalist economic system that places the value of human life above materialistic priorities such as capital, property, and the accumulation of wealth

Exploring how public ownership of strategic energy assets can improve long-term stability while generating public wealth.

A fully open-source AI robot featuring natural conversation, autonomous navigation, computer vision, and a modular 3D-printed body.

An all-in-one platform for managing properties, direct bookings, and guest experiences.